American Transit's Financial Hole Widens to Nearly $1 Billion

Nearly two years after the ATIC insolvency story broke, the deficit at NYC's largest taxi and for-hire vehicle insurer has grown, not closed. Part 1 of a series on the path forward

Nearly two years ago, in August 2024, this publication elevated a story that had long been underreported. American Transit Insurance Company, also known as ATIC, the largest insurer of NYC taxis and TLC-plated for-hire vehicles (FHVs), controlling over 60% of one of the world’s largest for-hire transportation insurance markets, was deeply insolvent. Over $650 million insolvent. In simple terms, if American Transit needed to pay out all its estimated claims, it would be short by over half a billion dollars.

Major publications picked up the American Transit story: Bloomberg, The New York Times, The Wall Street Journal. Given the wave of prominent coverage, we assumed it marked the beginning of the end for ATIC, or at the very least the end of the status quo. Surely, we thought, an insurer this insolvent, now officially acknowledged and in the national and local media spotlight, would not be permitted to keep operating in New York, one of the most stringent states in the country in which to run an insurance company.

This is not too dissimilar from a regulator knowingly allowing a bank to keep operating when it cannot return its depositors’ money. Two things would likely follow. The depositors (bank’s customers) would tell everyone they know, post about it, line up at branches, and likely trigger a run on the bank. And the regulator, in any functioning market, would step in almost immediately.

It was only in 2024 that ATIC’s true financial condition, decades in the making, was fully and publicly acknowledged by the Department of Financial Services (DFS), the state’s insurance regulator.

Lawsuits were filed by and against American Transit. The New York City Council halved the no-fault (PIP) minimum coverage limit for city taxis and TLC-plated FHVs last year, to $100,000, a rare cut intended to disincentivize the fraudulent claims that ATIC and others have primarily blamed for runaway losses.

At the state level, historic action came this week. Today, Governor Kathy Hochul signed into law a substantive package of auto insurance reforms as part of the state budget, targeting fraudulent claims and clarifying the definition of “serious injury” for pain-and-suffering damages. This is the largest fraud-targeted auto insurance intervention New York has passed in decades, and it should provide genuine tailwinds for the entire NY auto insurance market on a go-forward basis, ATIC included.

It is also worth noting how the reforms got over the line. Uber spent more than $8 million in New York alone in support of the package, for two primary reasons. First, outside NYC, Uber itself carries the commercial for-hire coverage for its drivers across the state, and the reforms should lower its own go-forward costs. Second, Uber has its own direct grievance with American Transit. In March 2026, US District Judge Analisa Torres ruled that ATIC breached its duty to defend Uber in 23 lawsuits and ordered ATIC to cover Uber’s legal fees. The platform that built much of its lucrative, and highly profitable, NYC business on top of ATIC-insured FHVs has, more recently, been on the receiving end of American Transit’s deteriorating ability to meet its obligations.

That said, reforms of this kind generally work prospectively. They reduce future loss costs and may modestly affect certain open claims, but the bulk of ATIC’s reserve deficiency reflects losses already incurred, where the law at the time of loss is most relevant. ATIC can write better business tomorrow. The new reforms will not, on their own, fill the hole the company has dug over the past decades.

Our readers, and many others, know the above.

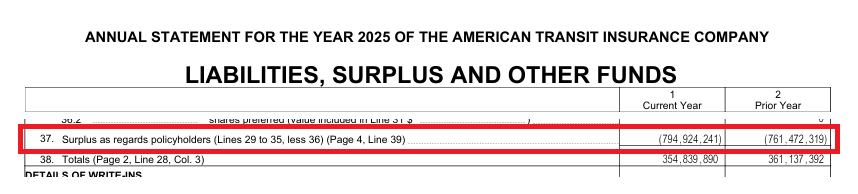

What may surprise them is this: American Transit’s insolvency has gotten worse, even as historic premium increases are pushed through. The company’s own filed policyholders’ surplus, the regulatory measure of solvency, has fallen to negative $795 million as of December 2025, from negative $761 million in December 2024. Over the same period, total premiums collected rose 14% to $419 million.

In other words, even as ATIC’s topline grows (and it will likely keep growing, given announced TLC liability rate increases), there is no visible bridge to the company making meaningful money anytime soon, let alone substantially reducing its deficit.

To make matters worse, the company’s own appointed actuary puts the true shortfall at over $1 billion, roughly $238 million beyond ATIC’s own estimate.

In my opinion, the amounts carried [at American Transit]:

A. Do not meet the requirements of the insurance laws of New York;

B. Are not consistent with reserves computed in accordance with accepted actuarial standards; and

C. Make an inadequate provision in the aggregate for all unpaid loss and loss adjustment expense obligations of the Company under the terms of its contracts and agreements.The Company’s $998,925,000 provision for unpaid losses and loss adjustment expenses is approximately $237,603,000 less than the minimum amount I consider necessary to be a reasonable estimate. This is the amount by which I estimate both the net of reinsurance reserves for losses and loss adjustment expenses and gross of reinsurance reserves for losses and loss adjustment expenses are deficient on an undiscounted basis. Using my reserve estimate, the Company’s statutory policyholders’ surplus would be -$1,032,527,241.

— Ronald T. Kuehn, Huggins Actuarial Services, Statement of Actuarial Opinion, American Transit Insurance Company (March 3, 2026)

This is not an outside critic, a competitor, or a plaintiff. It is the actuary American Transit itself retains, telling the regulator, in a sworn opinion, that the company’s reserves do not meet New York insurance law (yet again, but the number keeps getting larger).

Today’s piece is the first in a series of articles and videos that aim not only to provide a meaningful, technical financial update on the situation at American Transit and the broader NYC TLC insurance market, but to ultimately propose solutions.

We can acknowledge that American Transit may well be “too big to fail.” But we would argue it is not too big to shrink. This article, and the content that follows it, is not meant to be a hit piece on American Transit. We don’t see a point in that, at this stage.

Everyone understands the unusual history of how we arrived where we are. Dwelling on the “why” is not the best use of time, except where it provides context that informs the solutions we propose.

Article continues after advertisement

How Bad Is It?

Whether you believe the company’s or the actuary’s estimate, the conclusion is the same. Without significant regulatory action or a capital injection, ATIC is going to remain deeply insolvent for years. If the Department of Financial Services (DFS) allows ATIC to keep operating as an insolvent carrier, it could carry on for several years, as long as it has cash on hand to make near-term payouts. Again, that would be an astonishing status quo to let continue.

Yes, American Transit may well be “too big to fail.” But allowing an insolvent insurer to operate indefinitely violates two things at once: New York State’s insurance laws, and a more fundamental principle that underlies every developed insurance market in the world. An insurance company must hold enough capital to pay the claims it has agreed to cover. That principle is not ideological. It is what makes an insurance company an insurance company.

That an insurer of ATIC’s size is permitted to operate while failing both tests is, as far as we can tell, without precedent.

Consider the scale.

The appointed actuary’s shortfall of more than $1 billion is roughly 2.5 times ATIC’s annual premium base. In simple terms, ATIC is so insolvent that even if it generated 100% profit on every premium dollar it collected for a year, it would still owe more than it had earned. Of course underwriting margins in commercial for-hire transport are typically negligible, often negative. What profits exist in the industry come from the investment income insurers generate on the premiums they hold while waiting to pay out claims.

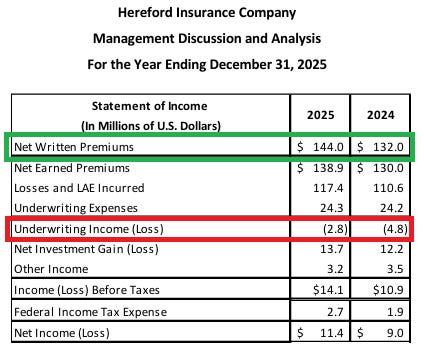

ATIC, and even its sole solvent competitor Hereford, typically lose money on the underlying for-hire transport risk they take on. For example, Hereford collected $144 million in net written premiums in 2025, the majority NYC taxi and TLC risk, and lost $2.8 million on underwriting. Only a $13.7 million gain on its investment portfolio carried Hereford to an $11.4 million net profit.

That context is essential, because ATIC operates the same line of business at roughly three times Hereford's scale and produces vastly worse results. On $418.6 million of net written premiums in 2025, and setting aside the appointed actuary's separate findings, ATIC posted a $58.5 million underwriting loss. A $9.4 million investment gain and a $14.7 million gain from "finance and service charges not included in premiums" offset some of that, but the company still finished 2025 with a $34 million net loss. ATIC collected over $400 million in TLC liability premiums and lost money on the year.

ATIC being insolvent to the tune of near a billion dollars is unprecedented. In our opinion, absent a state-facilitated bailout or capital injection, the company is insolvent by decades. Announced rate increases will help. The financial hole is too large for rate increases alone, or reforms, to close.

The blame, however, does not belong to American Transit alone.

How ATIC Got Here: Another Version

Before and since our original reporting, we have covered the NYC taxi and for-hire vehicle (TLC) insurance market in depth, sharing direct perspectives from the market’s leading voices:

Dan Bratshpis, Co-Founder & CEO of INSHUR

Gavriel Gavrilov, Owner of Next Century Insurance, a leading TLC broker

Luis Quevedo, CEO of NYAB Insurance, a leading TLC broker

Jeremy Moskovitz, EVP at Voyager Global Mobility, a large TLC rental fleet

Matt Daus, former Chair of the NYC Taxi & Limousine Commission

Steven Shanker, Litigation & Corporate Partner, Romano Law

Cira Angeles, CEO of L.A. Riverside Brokerage, a leading TLC broker

Beyond our published coverage and podcast, we are in constant contact with TLC insurance industry executives and stakeholders. Our fleet management business collectively oversees more than $500,000 in annual NYC for-hire liability premiums, and growing. And we created and publish the only dedicated TLC-specific insurance index, the AutoMarketplace Insurance Index (AIX).

We know the market, and we know the people who run it. With that context, in this first installment of the series, we are going to do something readers may find unusual: lay out an alternative history of how American Transit ended up here.

We do this for a reason. The solutions we will propose in later installments may strike some readers as counterintuitive, and perhaps even unfair to certain parties. That is because any honest solution to a problem this large requires understanding how it was built, who tolerated it, who benefited from it, and why none of those parties acted to stop it. Without that history, the proposals that follow will not make sense. With it, they will.

That alternative history runs roughly as follows.

New York needed someone to insure its taxis and FHVs. TLC liability is a notoriously difficult specialty commercial auto risk, and a very hard one to make money on. Regulators understood ATIC was insolvent but allowed it to keep operating because it kept coverage flowing to drivers and fleets.

The original logic for letting ATIC underprice was social. The goal was to keep insurance affordable for working-class NYC taxi and FHV drivers, who had few alternatives.

Over time, a near-total lack of oversight let things drift. Since ATIC was allowed to underprice, and likely to underestimate, its rates and expected payouts, it cemented a dominant market share. Decades of accommodation hardened into the “too big to fail” position ATIC occupies today.

Before the rise of e-hail apps, the insolvency was relatively contained. ATIC was insuring a well-defined niche, mostly full-time, experienced, commercially licensed drivers. New York tolerated the resulting financial situation because the affected population was small and the risk pool was knowable.

Uber and Lyft changed the math. As the app-hail platforms scaled, tens of thousands of new FHVs hit the road. The risk pool changed, with more inexperienced drivers and more part-timers, and ATIC’s pricing (and expertise) never caught up.

That same surge was a historic windfall for ATIC’s premium base. Insurers collect premium years before claims come due, so a fast-growing book provided the upfront working capital that kept ATIC operating long past the point at which the underlying economics had broken.

Without ATIC, Uber and Lyft could not have scaled in NYC. For the UberX and standard Lyft products, New York was the only major North American market where vehicle owners, not the platforms, carried the commercial for-hire coverage. That made NYC unusually profitable for the platforms. Uber itself has acknowledged on earnings calls that insurance is one of its largest expense category.

Then fraud broke the system. Rampant, unchecked fraud, arguably amplified by the e-hail model, produced losses on a scale the market had never seen, or at least multiplied already-bad industry losses across a far larger fleet.

ATIC’s story almost certainly also involves financial mismanagement, a topic we will examine in upcoming installments. But there is real evidence that its insolvency was knowingly tolerated for decades, and not just by the regulator. Uber and Lyft, the brokers, the fleets, and the drivers themselves all benefited from the arrangement.

Drivers and fleets got insurance they could afford. Brokers earned commissions. The platforms scaled on a coverage structure that made NYC unusually profitable for them. The regulator avoided the disruption of a forced wind-down. For most of the past decades, almost every active participant in the NYC TLC insurance market was, in some way, a beneficiary of ATIC being allowed to operate while insolvent.

The losers were the parties not in the room. Competitors, current and prospective, could not effectively compete or enter a market priced below their cost of capital, which is part of why ATIC’s market share never faced real pressure. And the parties who may ultimately bear the cost are the ones who had nothing to do with creating the problem: New York taxpayers, if a bailout is eventually required, and the drivers and passengers whose claims may be undercompensated, delayed, or poorly defended because the carrier on the policy could not actually pay what it owed.

That is the harder version of the alternative history. Almost everyone inside the system benefited from the accommodation while it lasted. The people who will pay for it are largely outside the system, and arriving late.

In our next article in this series, we will summarize a letter from Ralph Bisceglia, CEO and President of American Transit, to the New York Department of Financial Services, outlining what the company says it is doing to improve its financial position, and what it views as the root cause of its problem. We will also overview ATIC’s first quarter results, in which the company reports a net profit of $13.5 million, reducing its acknowledged deficit from $795 million to $784 million.

AutoMarketplace reports on, operates, and invests in New York City’s for-hire transportation (TLC) industry and the wider automotive mobility landscape.

AutoMarketplace.com is a market intelligence and fleet management platform for New York City’s for-hire vehicle ecosystem—delivering proprietary indexes (AYX, APX, AIX), real-time analytics, and fleet services across taxi medallions, TLC plates, and commercial insurance.

Check out AutoMarketplace on YouTube. Interested in advertising with us? Click here.

This is a real problem