☂️🚕 NYC TLC Insurance: 2023 Market Overview

☂️🚕 NYC TLC Insurance: 2023 Market Overview

With the annual NYC TLC insurance renewal season underway, we provide a 2023 update to our 2022 overview of the industry

Today, we wanted to share an updated 2023 version of our 2022 piece overviewing the NYC TLC liability insurance market ☂️🚕. The annual TLC insurance renewal period is underway with many of last year’s policies expiring on March 1st.

A lot has changed over the past 12 months from generational inflation to increasing interest rates which, among other things, greatly impacts the insurance industry.

Let’s briefly start with the basics again.

Why Are There Only A Few TLC Insurance Companies?

Most people appreciate and understand the fundamental value proposition of insurance. Basically, an entity collects money from a large group to help facilitate the payout of large one-off expenses, often related to catastrophes or rare incidences. Without insurance, most individuals and companies would not be able to financially navigate many life and business risks.

For example, if you own a house, you may pay $100 per month for home insurance that covers flooding in the off chance (i.e., 0.1%) your house gets flooded, resulting in $250,000+ of damages.

An insurance company calculates premiums based on sophisticated financial models (known as actuarial models). The company wants (& needs) to make sure the premiums they collect and invest, can payout expected claims and (hopefully) result in a profitable business.

In the example above, if the hypothetical 0.1% probability of your house flooding went up to 1%, it should make sense to you that your insurance premiums are going to go up significantly. In other words, the risk of your house flooding went up 10x from 0.1% to 1.0%.

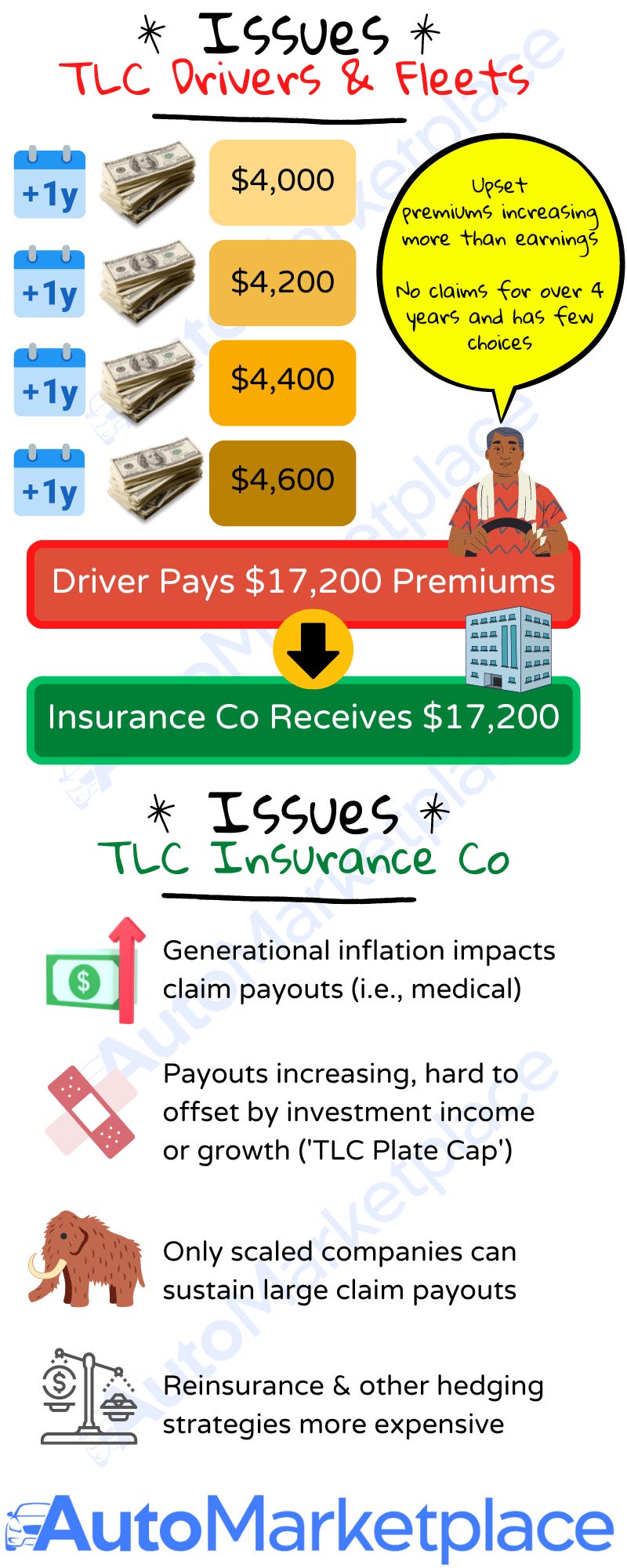

Below, we illustrate how the NYC for-hire transport insurance industry (aka TLC insurance industry) financial flows look like at a high level.

Some key issues are simply summarized below.

This can get much more complex with reinsurance structures etc., but that discussion isn’t required for a simple high level understanding of the NYC TLC liability insurance market.

The driver & fleet issues are easy to understand. In this example, a driver’s premiums keep going up, there is no history of claims and there are a few insurance options in the market to choose from.

The insurance company issues are less obvious. For example, rising inflation puts significant pressure on insurance company financials as claim payouts get much more costly to resolve (i.e., medical claims). In addition, the FHV License Pause (TLC Plate Cap) has also limited the growth of the industry. A market with capped & regulated growth plus tough macro dynamics, can be lucrative but also tough to navigate.

First Principles

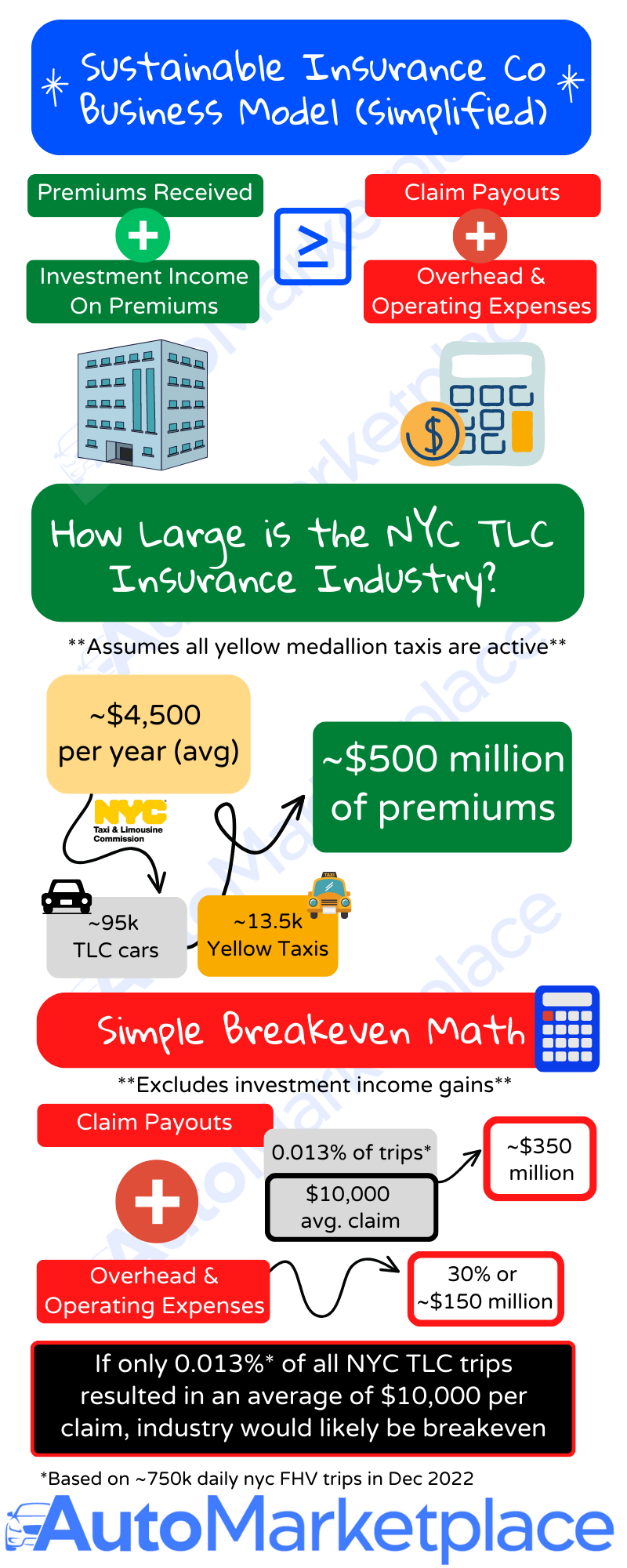

One must also go back to first principles and think about the nature of insurance. The only way to have a financially viable insurance company is to collect & invest premiums from enough people/companies who have no (or de minimis claims) to offset larger claim payouts and the operating expenses of the business.

The unfortunate story below illustrates the sort of risks involved in the for-hire transport insurance market. There are underlying reasons why State Farm, GEICO, Allstate, Progressive, etc aren’t in the TLC and taxi insurance industry in general…it’s RISKY. It’s also important to note that although Uber is being sued, ultimately an insurance company will be liable for a chunk of the payout, at least up to a policy’s liability limits. In NYC TLC market, those policy limits are $100,000 per person and $300,000 per incident.

Cost Of TLC Insurance & Need For Scale

For individual drivers, TLC liability policies tend to be between $3,500 to $5,000 annually. Corporate Fleet policies tend to range between $5,000 to $7,500 per vehicle, per year. We believe the TLC liability insurance industry is worth between $450 to $550 million in liability premiums, per year.

Based on the latest New York City Taxi & Limousine Commission data, there were over 100,000 active and insured for-hire vehicles, including yellow cabs. In December 2022, about 750,000 daily FHV and yellow cab trips were taking place in NYC, which if sustained would result in over 270 million yearly for-hire trips.

Remember, these ARE NOT full coverage policies that also cover physical damage and collision claims. Most NYC TLC driver and fleet policies are liability-only policies that don’t cover physical damage claims.

Given the TLC insurance market has limited growth now (TLC Plate Cap) and over 270 million trips (❗) that could result in claims 🤔, only a handful of companies collecting the majority of premiums could make the financial math work. For example, if you had an insurance company that insured 1,000 vehicles and was earning $4.5 million of premiums, a small number of bad accidents ($100k+ claim payouts) or incidents would bankrupt the company (claim payouts would be greater than premiums earned & investment income).

This is why the insurance industry, in general, lends itself to large companies that can distribute risk and costs due to economies of scale. Another way of saying this, is the more premiums a company can collect, the more risk they are able to distribute. There is something to be said for quality over quantity, but inherently an insurance company must have scale.

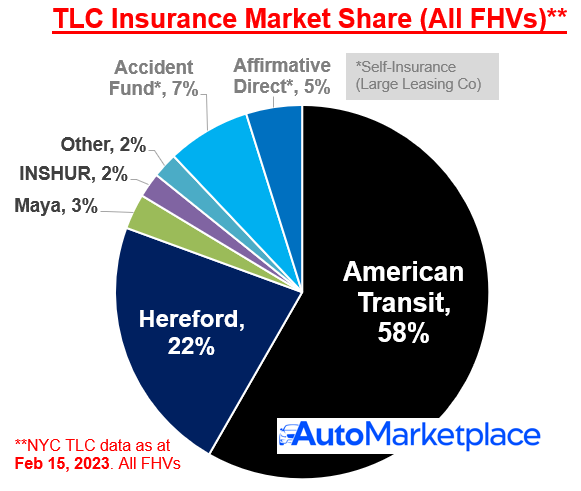

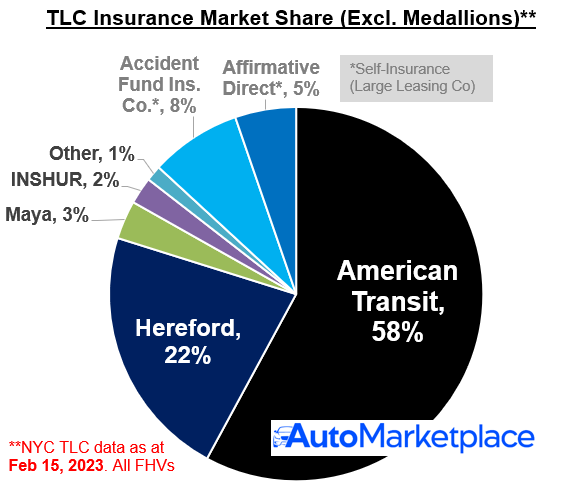

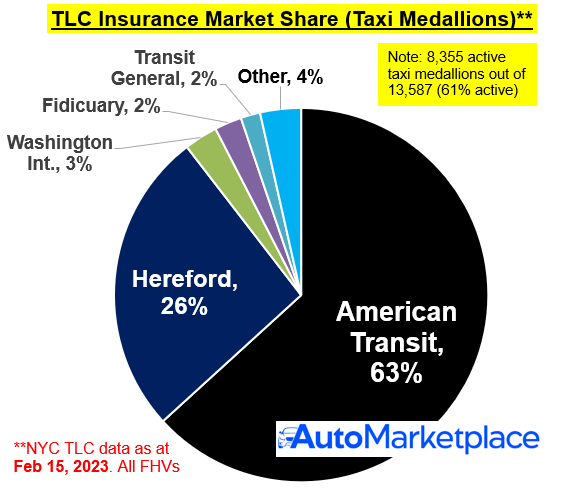

Who Are The Largest Players in NYC TLC Insurance?

Below we share a market share breakdown of the largest TLC liability insurance providers in NYC.

Remember our previous points above related to the inherent need for scaled players when contextualizing these market shares. We believe the market can only support a handful of companies. However, that doesn’t mean we don’t think the status quo can improve.

INSHUR & Maya Could Exit TLC Insurance Soon

Before we conclude this piece, it’s also worth noting #3 & #4 TLC liability insurance companies Maya Assurance and INSHUR currently only have 3,109 and 2,186 active liability policies, respectively. We think these companies may exit the TLC insurance industry soon as they lack the necessary scale. Both companies have lost hundreds of policies over the last 12 months.

Concluding Thoughts

Conceptually there are a few “high level” ways, outside of creating a new insurance company (not easy), to combat increasing insurance costs as a NYC TLC driver or fleet. Given shared cost headwinds faced by insurance companies, from rising claims costs to increasingly expensive reinsurance agreements, the best near to medium term solutions, in our view, to minimize insurance costs are:

Earn more money relative to insurance costs (less expense as a % of income)

Lower insurance costs by avoiding at-fault accidents and driving violations that result in points

As we’ve mentioned before, the TLC driver minimum pay formula makes an honest attempt at addressing (1), but uses a very generic inflation index. Given TLC liability insurance costs are easily trackable, this cost should be incorporated into TLC driver minimum pay calculations. With regards to (2), NYC TLC drivers should continue to drive defensively and carefully. In addition, having a dash camera is not only a way to get an insurance discount, but can also help drivers protect themselves against claims made against them.

As always, let us know your thoughts in the comments section below or by emailing us at info@automarketplace.com.

AutoMarketplace.com NYC covers the for-hire transportation industry and automotive news. Check out AutoMarketplace.com on YouTube ▶️

How to apply for electric plates for individual drivers